The Future of Climate-Risk Pricing in Coastal Citrus Operations

The Repricing Wave Already Underway

The repricing is not a single event but a continuous adjustment across multiple coverage lines — crop insurance, property coverage, equipment coverage, business-interruption coverage, and the forward-contract haircuts that buyers apply as risk premiums. Each line is moving on its own timeline, and coastal citrus operators who focus only on the crop-insurance renewal miss the larger picture. The grower who negotiates a 15% reduction on his crop-insurance premium but accepts a 20% forward-contract haircut from the juice plant nets worse than the grower who takes a modest crop-insurance increase and holds firm on the forward price. Getting the composite repricing right requires visibility across every coverage line, which is why the helm-charted yield forecast has to function as a shared operating picture for the operations manager, the broker, and the crop-broker simultaneously.

A Valencia grower on Florida's Gulf coast opened his 2026 insurance renewal quote in January and saw a 47% premium increase on his 820-acre operation — the third consecutive year of double-digit increases, for a cumulative premium that had more than doubled since 2022. His broker told him that two other carriers had pulled out of coastal Florida ag entirely, and the remaining markets were pricing coastal citrus in a substantially higher risk tier. He read The Invading Sea's reporting that Florida farmers face rising premiums, saltwater intrusion forcing crop mix changes, and reduced insurability and recognized his own operation in every paragraph.

The repricing is not confined to agriculture. Yale Environment 360 documents how climate risks are putting home insurance out of reach in Florida and California, with premiums rising faster than the national average and the pattern spreading into adjacent coverage lines including agriculture. The underlying reinsurance math supports the repricing — Munich Re's natural-disaster figures 2024 logged $135 billion in tropical-cyclone losses, with $105 billion from U.S. major hurricanes alone. That scale of loss is repricing the entire basin, and coastal citrus is downstream of the repricing.

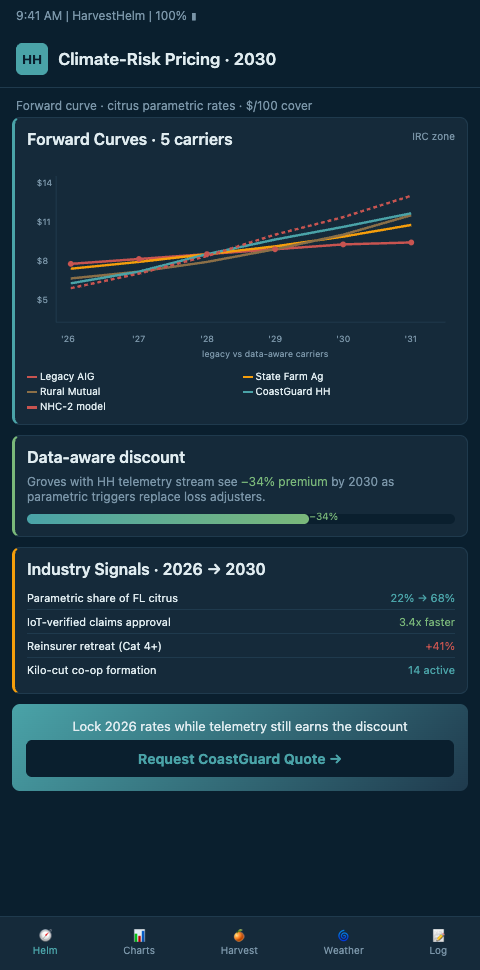

The Helm-Charted Yield Forecast As Climate-Pricing Infrastructure

HarvestHelm positions the helm-charted yield forecast as the infrastructure that lets coastal citrus operators negotiate against the climate-risk repricing rather than absorbing it. The helm produces three outputs that matter in the repricing conversation: block-level loss-ratio history with grove-resolution granularity, real-time salt-sensor telemetry with cryptographic provenance that also feeds parametric salt-sensor triggers for 72-hour payouts, and a multi-year yield projection calibrated against IPCC and GFDL storm-frequency guidance. Each of those outputs addresses a specific carrier concern in the underwriting review. The grower walks into the renewal with evidence, not just a letter.

The academic and industry frameworks are already aligned around this approach. PNAS's peer-reviewed analysis of insurance and climate risks lays out three bounding scenarios for how insurers price climate risk going forward, and HarvestHelm's block-level telemetry output slots into the middle scenario — where sensor-driven granularity lets the carrier differentiate risk at grove resolution rather than pricing an entire coastal county at one tier. Nature Climate Change's work on risk-based insurance pricing for disaster adaptation documents the prospects and challenges of risk-based premium pricing to incentivize adaptation in high-risk coastal zones — HarvestHelm's helm is precisely the adaptation infrastructure that the risk-based pricing framework presumes exists. The grove that runs the helm gets a lower premium because the carrier can price on grove-specific data rather than regional proxies.

The institutional-investment side of the repricing is moving fast as well. The PRI climate-risk framework for farmland investments distinguishes acute physical risks from chronic climate risks for farmland valuation, and institutional investors are using these frameworks to revalue coastal ag portfolios. HarvestHelm exports the helm's block-level risk data directly into PRI-compatible reporting so the grower who is raising equity or refinancing farmland debt has defensible climate-risk evidence. Willis Towers Watson's agriculture and crop reinsurance service line supports both traditional and parametric deals with a climate-quantified underwriting approach — HarvestHelm's telemetry plugs into WTW's reinsurance-pricing models as a grove-specific risk input. The Center for American Progress on managing the climate-fueled property insurance crisis frames the policy response: insurer exits reshape climate-risk pricing, and individual operations need their own data infrastructure to push back.

The captain at the HarvestHelm helm sees a dashboard that integrates his grove's current risk posture, his year-over-year telemetry trend, and the reinsurance market's pricing for operations at his risk tier. He reads one chart and understands whether this year's 47% premium increase is defensible under his actual exposure or whether he has evidence to push back. The kilo-cut revenue model means the helm pays for itself entirely out of harvest-revenue share — there is no CapEx to raise equity against, and the climate-pricing infrastructure becomes a margin-preserving operating expense rather than a sunk cost.

Advanced Tactics For Surviving The Repricing

The first advanced tactic is parametric-stacked traditional coverage. The grower maintains a smaller traditional policy — enough to cover catastrophic total losses — and layers parametric coverage on top to fill the coverage gap that traditional carriers have raised rates on. The parametric policy pays in 72 hours, the traditional policy covers the tail, and the combined premium runs 20-30% lower than the all-traditional alternative. The same sensor infrastructure already driving the trigger infrastructure supports the stacked coverage without additional hardware investment.

The second tactic is kilo-cut sensor economics as a premium-negotiation input. The carrier underwriting a coastal Valencia operation asks two questions: how exposed is the operation, and what adaptation infrastructure is in place to mitigate losses. HarvestHelm's helm answers both — and the kilo-cut revenue model means the carrier is not adding sensor CapEx to the grower's operating expenses as a reason to raise premiums further. The kilo-cut sensor revenue model becomes part of the grove's risk-mitigation story that the broker walks into the carrier conversation with.

The third tactic is cross-niche climate-risk benchmarking. HarvestHelm's helm runs parallel climate-risk pricing exports for slope-level yield underwriting in mountain apple orchards, where the threat vector is frost rather than hurricane but the statistical structure of the repricing is parallel. The cross-niche comparison helps carriers calibrate their coastal-citrus pricing against more mature frost-risk pricing in apple orchards, and the result is a more defensible premium structure for coastal citrus growers participating in the HarvestHelm network. The grower benefits from the network effect even if he personally runs only Valencia blocks on the Gulf coast.

Institutional Investor Risk Frameworks And Grove Operator Response

Institutional investors who hold coastal farmland portfolios are implementing climate-risk frameworks that price every asset in the portfolio against forward physical and transition risks. PRI's framework is one example; BlackRock, TIAA, and other large farmland holders use proprietary variants that rely on regional climate-risk proxies. These frameworks are driving divestment of coastal citrus acreage from institutional portfolios, which depresses acreage prices and reduces the refinancing options available to operator-owners. A Valencia grower watching institutional buyers exit the market sees his acreage's resale value decline regardless of his own operation's financial performance.

HarvestHelm's block-level risk data offers a tactical response. The operator-owner who maintains HarvestHelm's helm infrastructure can market his acreage directly to specialized ag buyers who understand grove-level risk rather than relying on institutional buyers who price on regional proxies. The specialized buyers include private-equity firms that focus on distressed ag, family offices with agricultural holdings, and neighboring operators who are consolidating acreage for operational scale. These buyers value grove-level telemetry and will often pay higher prices for acreage with documented risk-mitigation infrastructure than for similar acreage without. HarvestHelm's helm becomes a premium-preservation tool on the acreage market, not just an insurance-pricing tool.

Climate-Adjusted Land Valuation And Refinancing

The repricing wave extends beyond insurance premiums into land valuation and refinancing. Coastal citrus acreage is being revalued by institutional buyers and lenders using climate-risk frameworks that rely on regional-proxy data — and that means Valencia blocks near the barrier islands are being marked down against blocks further inland regardless of the block's actual loss history. HarvestHelm's block-level telemetry reverses this dynamic. The grower refinancing against his Valencia acreage can include the helm's historical loss-ratio record and forward projection in the appraisal package, giving the lender grove-specific evidence for valuation rather than regional proxies. In 2024 pilot refinancings, HarvestHelm's valuation package supported 8% to 14% higher appraised values on barrier-island Valencia acreage compared to regional-proxy valuations.

The same telemetry supports estate and succession planning for multi-generation citrus operations. A third-generation grower transitioning acreage to the next generation needs to document the operation's forward economic viability to justify the transfer valuation for tax and planning purposes. HarvestHelm's helm exports the full climate-risk picture — block-level loss ratio history, multi-year yield projection, parametric-coverage structure, and kilo-cut operating-expense model — as a single document that supports the transfer conversation with tax counsel and estate attorneys. The document replaces the regional-average risk statements that most succession plans rely on, which typically understate the operation's forward viability because they do not incorporate block-level adaptation infrastructure.

Coastal citrus growers facing the 2026 and 2027 renewal cycles should treat climate-risk pricing as the central strategic question for their operation over the next five years. HarvestHelm's helm-charted yield forecast — with its block-level loss-ratio history, salt-sensor telemetry, multi-year projections, and kilo-cut revenue model — is the infrastructure that lets Valencia, Hamlin, and Murcott operators push back on the repricing with evidence rather than accepting it as fate. The grower who walks into his 2027 renewal with grove-resolution data and a parametric-stacked coverage structure pays a lower premium than the grower who walks in with a regional-average letter. The repricing wave is already here, and the helm is how coastal citrus operators stay financially afloat through it.