Building a Parametric Insurance Trigger From Salt Sensor Telemetry

Why The 18-Month Payout Is Broken

A Valencia grower in DeSoto County watched federal disaster relief arrive for his Ian-damaged 2022 crop in March 2024 — 18 months after the storm. The relief check covered roughly 40% of his actual loss, and the reconciliation paperwork consumed two full months of his operations manager's calendar. Meanwhile, the parametric program a neighboring grower had signed up for paid out in 72 hours after Ian's wind-speed trigger fired, with no loss-adjustment field visit and no proof-of-loss photography. That 18-month-versus-72-hour payout delta is driving coastal citrus growers toward parametric products at a pace that reinsurers are struggling to service.

The market movement is already visible. Swiss Re reports the parametric agriculture market growing 15-20% annually versus 5% for traditional products, with soil moisture, rainfall, and NDVI as the standard trigger indices. But salt-sensor triggers are where coastal citrus needs the structure to go next — wind-speed triggers miss the salt-aerosol damage that does not track wind speed cleanly, and NDVI triggers lag by weeks because vegetation response to salt deposition takes 5 to 14 days to show up in satellite indices. The trigger needs to fire on the salt exposure itself, measured at the grove, and validated against UF/IFAS damage thresholds: 2,200 ppm at root or 1,500 ppm foliar spray can kill citrus.

The Helm-Charted Yield Forecast As A Parametric Trigger Engine

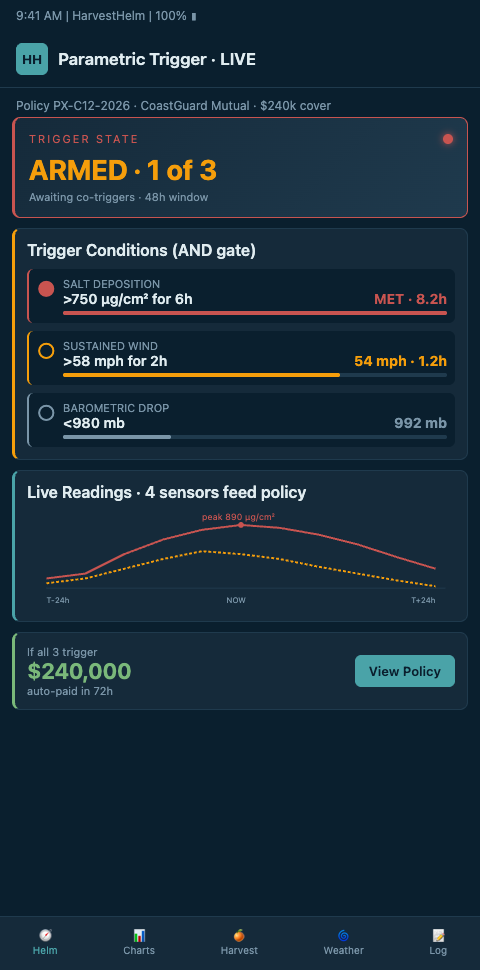

HarvestHelm is structurally well-suited to feed parametric insurance triggers because every sensor the helm runs is already calibrated, timestamped, and auditable — the same salt-aerosol probes that fire the hurricane-hour early warning beacon double as the parametric-payout trigger source. Because the sensor network rides on a kilo-cut sensor revenue contract, the grower pays nothing upfront for the trigger infrastructure — the same probes serve both the helm's harvest-save logic and the parametric payout. The helm-charted yield forecast exports a continuous telemetry stream that a parametric policy can reference via API, with cryptographic provenance the insurer can trust. The yacht-style helm becomes the trigger engine, not just the operations dashboard.

Trigger design is where most parametric salt products fall apart. The peer-reviewed NHESS 2025 systematic review of satellite and sensor-driven index insurance lays out the trigger-design methodology: the trigger must be measurable, objective, and tied to loss with low basis risk. HarvestHelm's standard trigger fires when the 48-hour integrated salt-aerosol exposure at the grove crosses the UF/IFAS 2,200 ppm root-zone threshold or the 1,500 ppm foliar threshold, measured by at least three in-grove probes with multi-source concurrence from AERONET and MODIS. That multi-source trigger cuts basis risk — the gap between the trigger firing and actual grove damage — because the insurer can audit all three source streams for agreement.

The underlying actuarial methodology is well-established. The ASTIN 2025 paper on parametric crop insurance pricing against bimodal yield distributions provides the pricing framework for parametric crop products against historical bimodal yield — which is exactly the distribution coastal citrus shows, with high-yield years interspersed with hurricane-loss years. HarvestHelm's helm-charted yield forecast exports both the real-time trigger stream and the historical block-level yield distribution, which lets the insurer price the trigger accurately. Swiss Re's comprehensive parametric insurance guide documents the structure, basis-risk management, and trigger-design primer that underlies this pricing work.

The insurer-side infrastructure is maturing around sensor-based products. Munich Re's parametric solutions for agriculture offers pre-defined triggers from third-party sources, including examples like Cat-3 hurricanes within 30 miles of insured — HarvestHelm's salt-sensor trigger is a more granular variant of the same structure. Arbol's parametric crop insurance platform uses AI-based underwriting against NOAA, NASA, and ESA data with payouts on predefined weather triggers, and HarvestHelm's telemetry plugs into Arbol's data-ingestion interface as an additional sensor feed. Descartes Underwriting writes sensor-based parametric hail, frost, and tropical-cyclone products using 80+ data sources including NOAA and IoT sensors — HarvestHelm's salt-aerosol feed slots directly into the Descartes underwriting stack as a citrus-specific trigger source.

Advanced Tactics For Parametric Trigger Design

The first advanced tactic is dual-threshold triggering. HarvestHelm designs the parametric contract with a lower-band trigger at 1,500 ppm foliar (partial payout) and an upper-band trigger at 2,200 ppm root-zone (full payout) — which reflects the bimodal damage curve coastal citrus actually experiences. A partial salt-spray event that defoliates a Valencia block without killing it triggers the lower band and pays out 40% of the coverage. A full salt-spray blackout event that kills a percentage of the block triggers the upper band and pays 100%. That graduated trigger structure reduces basis risk and matches the grower's actual loss distribution — and because the underlying sensors ride the kilo-cut contract, the grower never capitalizes the trigger infrastructure separately.

The second tactic is multi-peril trigger stacking. The salt-sensor trigger fires on salt exposure, but coastal citrus operations also face wind, freshwater flush, and fruit-split threats post-storm. HarvestHelm's helm can feed a stacked parametric policy where the salt trigger is one element, a wind-speed trigger is another, and a freshwater-flush trigger is a third. The grower pays one premium for the stacked coverage and receives payouts on whichever trigger fires first. Tie this stacking approach to coastal climate-risk pricing evolution to see where parametric-product design is heading over the next five years.

The third tactic is cross-niche trigger portability. HarvestHelm's parametric trigger architecture is not coastal-citrus-specific — the same multi-source concurrence and cryptographic provenance structure works for oasis insurance mispricing of sandstorm risk in date palm operations, where the trigger fires on PM10 particulate exposure rather than salt-aerosol. The statistical underwriting benefits from cross-niche validation, which in turn lowers the underwriter's basis-risk loading on coastal citrus triggers. The grower pays less for the parametric product because the insurer is more confident in the trigger calibration.

Basis Risk And Trigger Calibration Against Historical Events

Basis risk — the gap between the trigger firing and the actual grove damage — is the parametric-contract equivalent of a false-positive beacon. A trigger calibrated too loose will fire on non-damaging events and pay out the insurer's capital on losses that did not materialize, which the insurer prices into the next year's premium as a surcharge. A trigger calibrated too tight will fail to fire on damaging events and leave the grower without coverage when it matters. HarvestHelm's calibration methodology walks the historical record of Ian, Milton, Irma, and Matthew through the proposed trigger logic and measures how each storm would have fired or failed under the candidate thresholds, then iterates the thresholds against the documented grove damage from each storm to minimize basis risk in both directions.

The calibration exercise is transparent to the grower and the insurer, which matters for trust-building in a product category that depends on aligned expectations. Both parties see the trigger-versus-damage scatter plot across the historical storm record, and both parties sign off on the calibrated thresholds before the policy binds. That transparency is what allows parametric products to price competitively against traditional coverage — the insurer is confident the trigger is well-aligned with loss, and the grower is confident the trigger will fire when damage materializes. HarvestHelm's kilo-cut revenue model fits this collaboration well because the vendor has no incentive to game the calibration in either direction; a well-calibrated trigger means more harvest saves, more harvest revenue, and more kilo-cut earnings for HarvestHelm.

Sensor Audit Trail And Dispute Resolution

The single biggest failure mode for parametric contracts is the dispute that follows a trigger event — either the insurer contesting whether the trigger actually fired, or the insured contesting whether the measurement was valid. HarvestHelm's audit trail closes this failure mode structurally. Every sensor reading is cryptographically signed at the device level before it leaves the gateway, timestamped against GPS-synchronized UTC, and archived in a write-once log that the insurer can pull on demand. The log includes the firmware version, calibration date, and maintenance history for each probe, so the insurer can verify the measurement pipeline end-to-end without trusting the grower's assertion. When a trigger fires, the insurer receives the audit bundle along with the payout request, and the 72-hour payout window accommodates the review. That structure is the difference between a parametric contract that pays cleanly and one that lands in arbitration.

The audit trail also supports insurer-driven calibration updates. After each hurricane season, the insurer reviews the trigger firings against the actual grove damage documented by the packinghouse and the FDACS claim record. Blocks where the trigger fired but damage was minimal, or where damage was severe but the trigger did not fire, feed the calibration update for the next season. HarvestHelm's helm accepts insurer calibration updates directly into the trigger threshold logic, which means the parametric contract becomes a living instrument that sharpens each year rather than a static threshold that drifts out of alignment with ground truth. The grower benefits because the basis risk shrinks year over year, and the insurer benefits because the trigger's predictive accuracy improves with every season of data.

Coastal citrus growers still operating on the 18-month federal-disaster-relief payout timeline are leaving money on the table — the parametric market is maturing fast, the UF/IFAS threshold data is public, and the only missing piece for most groves is an audited sensor network that feeds the trigger. HarvestHelm provides that sensor network on a kilo-cut basis, so the grower pays nothing upfront for the trigger infrastructure and the insurer gets audited telemetry from day one. Valencia, Hamlin, and Murcott operators who have been hit by Ian, Milton, or any future storm should be asking their broker about parametric salt-sensor products this renewal cycle. The 72-hour payout is the new standard.