Why Oasis Insurance Markets Misprice Sandstorm Yield Risk

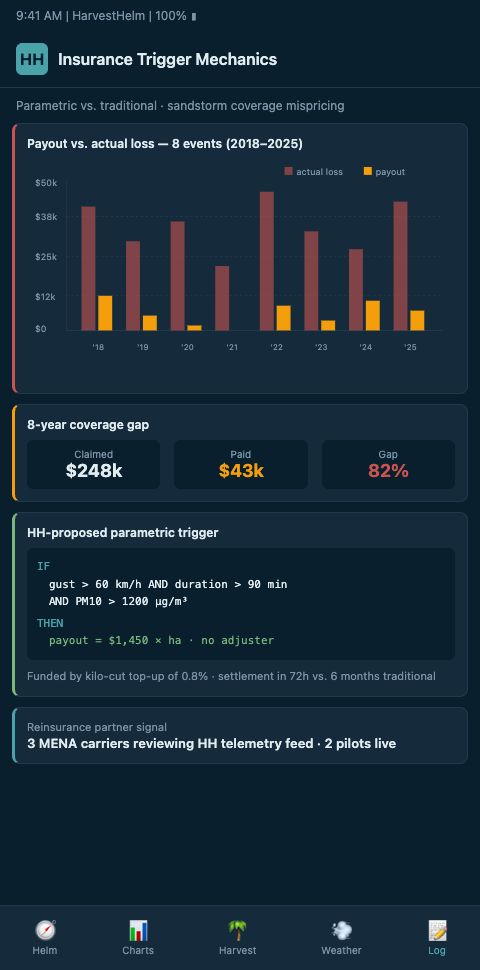

The Pricing Gap in Oasis Crop Insurance

Agricultural insurance markets in MENA, North Africa, and the Coachella Valley have struggled for years to price sandstorm risk on date palm crops. The underlying problem is structural: underwriters price from historical loss data aggregated at regional or provincial scale, but sandstorm exposure at the parcel level varies by a factor of four or five depending on wadi orientation, upwind source geography, and canopy geometry. A grower whose actual risk is 40% below regional average pays the same premium as a grower whose risk is 60% above regional average, because the underwriter cannot see the difference.

Swiss Re's analysis of parametric agricultural insurance documents the parametric market growing 15-20% per year against traditional crop insurance at 5%, driven explicitly by climate-risk mispricing gaps. Their companion piece on strengthening crop insurance with digital solutions identifies the data gap between traditional crop insurance and smallholder risk exposure as a primary driver of coverage gaps.

The Agricultural and Food Economics paper on weather index insurance for drought risk in sub-Saharan Africa identifies basis risk — the mismatch between index triggers and actual farm-level losses — as the key barrier to index insurance uptake. For date palm cultivators, basis risk manifests specifically as sandstorm payouts that trigger on regional wind-speed averages while individual parcels either escape the storm or take disproportionate damage. Growers who see their neighbor receive a payout for a storm that hit their block harder lose trust in the instrument, and the market's credibility erodes.

The ScienceDirect study on soil-dust storm impact on farm income quantifies rain-fed farmer income loss per dust hour — ground-truth data that traditional underwriters typically do not have access to when pricing oasis policies. The World Bank MENA dust storm report monetizes MENA dust storm crop damage at hundreds of millions per event, providing the baseline for reset underwriter premiums — but only if the underwriter has sensor-fed loss data to work from.

The Helm-Charted Yield Forecast as Insurance Infrastructure

HarvestHelm's helm-charted yield forecast is not an insurance product, but it produces the sensor-backed loss record that makes properly priced parametric insurance possible. The yacht dashboard's real-time storm tracking, parcel-level dust exposure logs, and fruit-set impact attribution create a verifiable event record that an underwriter can trust. When a parametric policy triggers on a haboob, the helm's sensor record corroborates both the event and its parcel-specific severity — reducing basis risk and tightening the payout calibration.

Munich Re's parametric solutions playbook for agriculture documents the reinsurer's framework for indexing haboob and wind-speed triggers with payout structures calibrated to sensor-derived loss data. The Springer review of weather index insurance advancements surveys how high-resolution satellite and IoT data is reshaping index insurance pricing toward precision — which is exactly the shift a parcel-level telemetry stack enables for date palm cultivation.

Our contribution to the insurance ecosystem runs in three layers. First, continuous parcel-level telemetry generates a verified event log — wind speed, dust AOD, humidity crash timing, duration of conditions outside the cultivar's tolerance window — that an underwriter can price against. Second, the yield forecast attributes fruit-set loss to specific events, so a policy payout can correspond to a specific sandstorm's contribution to loss rather than an aggregate seasonal shortfall that may include other causes. Third, the dashboard surfaces insurance-trigger proximity in real time, so a grower watching a haboob approach can see whether their policy is about to pay out and plan accordingly.

J-PAL's review of index insurance evidence documents that insurance uptake depends heavily on product design clarity and trust — both of which improve when the underlying trigger is corroborated by grower-owned sensors. Growers who can see their own telemetry alongside the policy trigger have more confidence in the contract than growers staring at a regional index they cannot verify. We cover the smallholder economics of this in our companion piece on revenue-share smallholders, where insurance payouts complement the kilo-cut structure during catastrophic seasons.

Advanced Tactics: Fixing the Basis-Risk Problem

The first advanced move is triangulated event attribution. A parcel-level sensor reading alone is not bulletproof — a faulty anemometer or a miscalibrated AOD sensor could generate a false trigger. We triangulate sandstorm events against satellite dust AOD retrievals, regional WMO SDS-WAS node outputs, and the grower's own downwind neighbor telemetry. An event that corroborates across all three sources feeds a high-confidence insurance trigger. An event with single-source detection fires a watch rather than a payout condition. This triangulation discipline mirrors the satellite-fusion architecture we described in our post on dust plume fusion.

The second tactic is policy-instrumented operations. For growers with parametric coverage, we configure the yacht dashboard to surface policy-trigger proximity alongside operational alerts. If a grower's policy triggers at 85 mph sustained winds for 30+ minutes with AOD above 0.8 for 60+ minutes, the helm shows the current reading against that threshold in real time. The grower can make evacuation and pollination-rescue calls with the insurance payout horizon visible, which changes the operational calculus around burning emergency crew capacity.

The third tactic is export-grade audit integration. Sandstorm damage to export-grade Medjool, Deglet Noor, Barhi, or Zahidi can produce insurance claims that require documentation chains back to the storm event. The helm's event log supports export audit reconstructions, so a claim or dispute can be backed by the continuous sensor record. We explore the export-audit side of this in sandstorm export audits, where the same data provenance that fights mispricing also strengthens trade-dispute claims.

The fourth tactic is cross-niche underwriting collaboration. The basis-risk problem is not unique to sandstorms. Parametric salt trigger in coastal citrus groves faces the same structural mispricing gap — regional hurricane indices that miss parcel-level salt deposition, just as regional wind indices miss parcel-level sandstorm exposure. Our cross-crop telemetry stack gives reinsurers a unified sensor language to price parametric products against, reducing the per-crop engineering burden and accelerating market entry for properly priced oasis coverage.

The fifth tactic is transparent actuarial sharing. When we supply sensor data to underwriters for policy pricing, we also disclose the aggregated patterns back to participating growers through the yacht dashboard. Growers can see whether the current season's dust-exposure profile is running above or below the underwriter's prior-season assumptions — information that lets them assess whether their premium is still fairly priced mid-season or whether renewal negotiations are in order. Transparent sharing of actuarial signal is what turns insurance from a black-box expense into a legible operational tool.

The sixth tactic is multi-trigger policy stacking. A well-designed parametric date-palm policy does not depend on a single wind-speed threshold — it stacks multiple triggers that correspond to distinct physiological damage mechanisms. Sustained winds above a cultivar-specific threshold for a defined duration address mechanical spathe damage; AOD above a threshold for a defined duration addresses pollen viability loss; humidity drop below a threshold during receptivity addresses stigma desiccation. Each trigger has a distinct payout weighted by its typical loss contribution. The helm's multi-sensor stack natively supports each trigger with corroborated measurement — making stacked-trigger policies feasible in ways single-index policies were not.

The seventh tactic is event-specific payout acceleration. A traditional crop insurance claim can take 4-8 months to settle — during which time the grower must absorb the cash-flow gap from a bad harvest. Parametric products with sensor-corroborated triggers settle within 30-60 days of the event because the trigger verification is automated. Our event-log structure is designed for this accelerated settlement; underwriters receive a sensor-backed event package within 72 hours of storm passage, and claim processing proceeds on a timeline that actually supports the grower's working capital. Faster settlement is, in many cases, as valuable as the payout itself.

The eighth tactic is catastrophic-event pooling across oases. A single catastrophic khamsin affecting multiple oases within the HarvestHelm network creates correlated insurance claims that strain individual underwriters but can be pooled across a reinsurance layer. Our sensor network provides the correlated event evidence across all affected oases, supporting efficient reinsurance pricing and payout. This pooling is structurally difficult without a unified sensor architecture, because each underwriter otherwise depends on separate verification chains for each grower — driving up the per-policy administrative cost and pushing premiums higher than the underlying risk justifies.

Price the Storm, Not the Province

If you've ever paid for crop insurance that treated your specific parcel as a statistical average of your entire province, you know the basis-risk problem from the wrong end. HarvestHelm's sensor-backed event record gives you and your underwriter a parcel-level ground truth for every khamsin, haboob, and dust surge that crosses your Medjool, Deglet Noor, Barhi, or Zahidi blocks — so parametric policies can price and pay out on what actually happened to your palms, not what averaged across a 70-kilometer grid cell. Because our kilo-cut pricing earns only on successful harvest tonnage, we have incentive to make every storm event verifiable and every yield attribution honest.

If you're evaluating parametric date-palm coverage or renegotiating a traditional policy, we'll supply your underwriter with the multi-season sensor record that resets the conversation from regional averages to your specific storm exposure. Join the parametric-underwriting waitlist before the next insurance renewal cycle, and on day one the dashboard will surface your parcel-level triangulated event log ready for submission to reinsurers at Munich Re and Swiss Re templates. Waitlisted Coachella and Tozeur operators who supplied triangulated records ahead of last renewal reset premium pricing against rutab-stage sandstorm exposure that the regional index had been averaging away across their Barhi and Medjool blocks.