How to Hedge Citrus Futures Against Salt-Damage Yield Loss

The Hedge Window Most Growers Miss

Orange Juice Futures Rise as Hurricane Milton Nears Landfall (FreshPlaza) documented the October 2024 price spike: FCOJ-A jumped 3.3 percent in the 48 hours before landfall as traders priced in supply disruption. Most coastal citrus growers, watching the storm rather than the screen, missed the ideal hedge window. By the time Milton made landfall, the futures had already partially baked in the expected yield loss, shrinking the protection value of a short hedge placed post-storm.

The window is narrow and unforgiving. FCOJ-A moved approximately 1.1 percent per day across the three trading sessions leading into Milton's landfall — a grove that placed a hedge 36 hours earlier than the last reasonable hedge moment captured an additional 1.5 to 2 cents of protection per pound of solids. On 325,000 pounds of solids exposure, that differential alone is $32,500 to $45,000. Growers who missed the window entirely, then tried to hedge post-landfall as initial damage reports appeared, found themselves locking in prices at the top of the short-term spike with limited downside protection remaining.

The mechanics matter. FCOJ-A Futures (ICE) is the benchmark contract for 15,000 pounds of orange solids, with every one-cent move equaling $150 per contract. A Florida grower expecting 50,000 boxes at roughly 6.5 pounds of solids per box has about 325,000 pounds of solids — enough exposure to justify roughly 22 FCOJ-A contracts as a short hedge. A three-cent adverse move without a hedge is $65,000 in uncompensated basis loss. A Cat 2 storm produces multi-cent moves routinely.

Hedge mathematics break down in two places for coastal groves. First, basis risk — the gap between FCOJ-A prices and the actual cash price you receive at the juice plant — widens during hurricane weeks. Second, salt-damage loss does not convert cleanly into the market-wide supply signal the futures contract tracks; a grove-specific 40 percent brix drop in your Valencia block may not move FCOJ-A at all if regional supply holds. The Index-Based Weather Derivative Product Note (World Bank) explains this basis-risk architecture in depth.

Helm-Charted Hedging: Layering Futures, Insurance, and Parametric Triggers

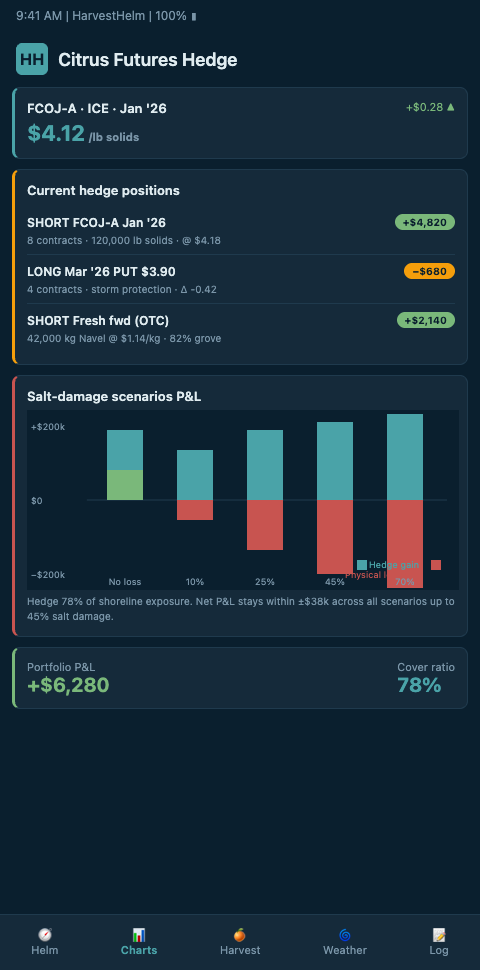

HarvestHelm treats grove hedging the way a yacht captain treats trip insurance, weather routing, and fuel pre-buys — three separate instruments that stack to cover different failure modes. The helm-charted yield forecast feeds all three layers, updating hedge sizing as the weather chart shifts and as grove sensor telemetry updates the salt-aerosol exposure model.

Layer one: FCOJ-A Futures (ICE) short positions sized to your solids exposure, placed when HarvestHelm flags a 5-day cone passing within 150 miles of your grove. The objective is not to predict the storm — it is to offset the systemic price risk during the window when orange juice futures will move on hurricane news. Size the hedge at 60 to 80 percent of your solids exposure, not 100 percent, because you still want upside if the storm weakens or curves.

Layer two: Hurricane Insurance Protection – Wind Index (USDA RMA). HIP-WI covers up to 95 percent of the underlying crop insurance deductible when a county lands in an NHC hurricane-force wind swath. Coastal citrus growers should stack HIP-WI on top of their APH or revenue policy as the first line against catastrophic wind loss. Pair that with Crop Insurance Policies Available to Citrus Growers (UF/IFAS EDIS CG096) options and, where eligible, the Whole-Farm Revenue Protection Plan (USDA RMA) — WFRP covers price and yield risk at 50 to 85 percent coverage levels with 80 percent premium subsidy once you insure at least two commodities.

Layer three: sensor-triggered parametric coverage. This is the new layer HarvestHelm's kilo-cut architecture enables. Our parametric salt trigger workflow shows how grove-installed salt-conductivity and wind-gust sensors can trigger payouts on objective thresholds — salt aerosol exposure crossing a pre-agreed ppm-hour integral, or sustained winds exceeding 60 mph measured on grove. Worsening Weather Igniting $25 Billion Weather Derivatives Market (Insurance Journal) documents the market growth: weather derivatives are scaling as growers look for coverage beyond the traditional crop-insurance complex.

The three layers interlock. Futures absorb the market-wide price shock. HIP-WI absorbs the county-level wind event. Parametric coverage absorbs the grove-specific salt damage that neither futures nor HIP-WI captures — the 40 percent brix drop in your Valencia block when the regional supply barely moves. HarvestHelm's helm-charted yield forecast sizes each layer against the live storm track and your grove's actual exposure, rather than leaving you to stack instruments manually under time pressure.

Advanced Tactics: Timing, Roll Costs, and Kilo-Cut Alignment

The timing question gets most growers in trouble. FCOJ-A contracts have limited liquidity, and placing a 22-contract short position 36 hours before landfall often moves the screen against you. The cleaner pattern is to establish a baseline hedge during the early season (June-July for Florida) sized to your expected solids exposure, then scale up when HarvestHelm flags an active track within the 5-day cone. That is how the kilo-cut revenue model stays aligned with your hedge — the tool earns on harvested kilos, so it has incentive to help you preserve both the physical fruit and the hedge P&L.

Roll costs matter on multi-month positions. If you hedge into the November FCOJ-A contract in July and the storm does not materialize until September, you may need to roll forward twice, paying the roll spread each time. HarvestHelm models expected roll cost against the probability-weighted hurricane frequency curve, so the hedge sizing accounts for the carry, not just the terminal value.

Cross-geography note: mountain apple growers face similar yield hedging contracts trade-offs when weighing fixed-price contracts against frost-exposed yield risk. The underlying architecture — layered instruments sized by sensor-derived risk — translates directly. Coastal citrus growers can learn from apple-orchard patterns, and vice versa.

Documentation is where hedges live or die. Every hedge placement needs a paper trail tying the position to the HarvestHelm helm-charted forecast that triggered it. When a claim hits HIP-WI or parametric coverage, that documentation accelerates adjudication and reduces dispute risk.

Sizing the Three Layers Against Your Actual Exposure

The three hedge layers do not all scale linearly with your grove's acreage — they scale with different exposure curves. Futures hedge sizing tracks expected solids output, which varies year to year with the yield forecast. A 50,000-box operation expecting a normal yield year hedges different contract volume than the same operation forecasting a drought-reduced yield. HarvestHelm's helm-charted yield forecast pushes the pre-season yield estimate into the futures-sizing calculation automatically, so the hedge matches the exposure rather than the acreage.

HIP-WI sizing tracks the underlying APH or revenue policy deductible, which is a county-level and policy-level decision independent of the storm forecast. The decision is whether to stack the HIP-WI rider on every county where your grove has exposure, and at what coverage percentage. Growers with grove spread across Hendry, Collier, Lee, and DeSoto counties should evaluate HIP-WI per county because county-specific hurricane-frequency math shifts the breakeven calculation.

Parametric sizing tracks the sensor-triggered event integral and the agreed payout schedule. HarvestHelm's kilo-cut economics work best when parametric coverage handles the grove-specific damage that futures and HIP-WI cannot capture. A typical parametric layer might pay out on sustained grove-measured winds over 55 mph lasting 90+ minutes, or salt-conductivity integrals crossing a rootstock-specific ppm-hour threshold. The payout scales with the event magnitude rather than with gross exposure.

Layer interaction matters on correlation. During a severe Cat 3 track, all three layers likely trigger: futures move on supply shock, HIP-WI triggers on county wind swath, parametric triggers on grove sensor readings. The aggregate payout should approach the total damage rather than over-pay, so the sizing ratios need to be tuned together rather than independently.

Monitoring and Rolling Position Management

Hedge positions require active management, not fire-and-forget placement. Weekly position reviews during hurricane season adjust for track development, futures price moves, and grove-level yield forecast changes. HarvestHelm surfaces the position-management checklist each week — contract expirations approaching, roll decisions needed, size adjustments triggered by forecast updates.

Basin activity tracking drives much of the review cadence. A quiet August with no Atlantic development may argue for rolling back the futures short layer to reduce carry cost, while an active August with multiple waves warrants full hedge coverage maintenance. Growers who let positions run on autopilot through changing conditions overpay for carry during quiet periods and underinsure during active ones.

Counterparty and Credit Considerations

Parametric coverage and custom weather derivatives introduce counterparty risk that traditional crop insurance does not have at the same level. A payout depends on the counterparty's solvency at the time of the trigger event, and large simultaneous triggers across a hurricane-exposed geography test counterparty capacity. Growers committing to parametric layers should evaluate the counterparty's AM Best rating, reinsurance backing, and historical payout performance before placing coverage.

Credit lines tied to the hedge stack also matter. A futures short position requires margin, and margin calls during adverse price moves can consume working capital precisely when the grove also needs liquidity for early-harvest crew dispatch. HarvestHelm's helm-charted yield forecast includes working-capital stress scenarios tied to hedge positions so growers know whether their cash position survives both the weather and the hedge-P&L simultaneously.

Stack the Hedge Before the Cone Crosses Your County

Florida Valencia, Hamlin, and Murcott growers operating inside 30 miles of the Gulf or Atlantic coast should not rely on a single hedging instrument. Layer FCOJ-A futures for market-wide price risk, HIP-WI for county-level wind events, and sensor-triggered parametric coverage for grove-specific salt damage — all sized against HarvestHelm's live helm-charted yield forecast. Book a hedge-stack working-capital review with us before the next Atlantic advisory and we will install sensors across your coastal blocks, load your existing positions, and size the three layers against the current forecast. Zero platform fee. The kilo-cut on successful harvest keeps the tool's incentive aligned with your grove's P&L through every active track of the season.