Building a Frost-Hour Futures Model for Variable-Elevation Orchards

The Risk-Transfer Gap for Variable-Elevation Orchards

A Hudson Valley apple grower running Honeycrisp at 1,650 feet, Gala at 1,850 feet, and Fuji at 2,200 feet faces three structurally different frost-hour exposures on one operation. Traditional crop insurance prices this as one average. The grower pays premiums calibrated to the mean risk but carries the variance of the extremes — a cliff-edge yield problem that no generic policy was built to solve.

Meanwhile, the weather derivatives market has been hedging temperature risk at institutional scale for years. The CME Group's introduction to weather derivatives documents the formal structure — heating-degree-day and cooling-degree-day contracts, location-specific reference stations, clear settlement formulas. GARP's analysis of weather derivatives shows that the market already hedges late-frost risk for breweries and utilities, setting the precedent for orchard frost-hour pricing. The technology exists. The market exists. What has been missing is an adaptation calibrated to the elevation-band structure of mountain apple orchards.

A frost-hour futures model is that adaptation. It prices the probability of accumulated frost-hours below critical thresholds at each elevation band across a defined policy window — typically bloom through June drop — and creates a tradeable structure that transfers the tail risk off the grower's balance sheet. For a 60-acre operation split across three elevation bands, that means three distinct contracts reflecting three distinct risk profiles.

Legacy crop insurance cannot price this way because it relies on county-level yield history aggregated across all elevations. A grower paying the county APH rate effectively pays a cross-subsidy that overprices their lower-risk blocks and underprices their higher-risk blocks — which is the worst of both worlds. The frost-hour futures model disaggregates this, letting each elevation band carry its own premium based on its own stochastic frost-hour distribution. High-elevation Fuji pays more; mid-elevation Gala pays less; the overall portfolio is priced accurately rather than averaged into uniformity.

Building the Model on a Helm-Charted Yield Forecast Foundation

Think of a frost-hour futures model the way a yacht captain thinks about buying passage insurance for a multi-leg cruise: each leg has its own risk profile (reef transit, open-ocean crossing, narrow channel), and the insurer prices each leg separately using historical data on losses in that specific geography. A helm-charted yield forecast gives the frost-hour futures model exactly that leg-by-leg risk data — not for ocean transits, but for elevation bands on a single ridge.

The model starts with a stochastic temperature process. ArXiv's temperature derivative stochastic model uses an Ornstein-Uhlenbeck-based framework for state-specific risk-averse derivative pricing, which adapts directly to frost-hour accumulation by tracking minimum temperature below defined thresholds (32F, 28F, 24F). MDPI Mathematics' stochastic drought derivatives framework shows the same math extends cleanly from arid to mountain contexts, so the same core engine prices both drought and frost.

HarvestHelm feeds the model three streams of data per elevation band. First, ten-plus seasons of block-level sensor data establishing the historical frost-hour distribution. Second, synoptic weather classification linking frost events to larger-scale patterns. Third, climate-drift adjustment bringing the prior distribution forward using the same multi-year chill-drift logic used in dormancy forecasting. The output is a probability distribution for frost-hours in the upcoming season, segmented by elevation band.

Each of these streams requires specific discipline. The historical frost-hour record has to be homogenized — sensor changes, relocations, and calibration drift can all create artificial discontinuities in the record that get confused with real climate signals. The synoptic classification uses reanalysis data (ERA5 or similar) to tag each historical frost event with the larger-scale pattern that produced it, allowing the model to weight recent years more heavily if the regional circulation patterns have shifted. The climate-drift adjustment applies a rolling bias correction so that a stationary-climate assumption does not underprice current risk.

The pricing math comes from basket derivative theory. MDPI Risks' work on pricing basket weather derivatives covers the multi-asset version of a single-temperature contract — directly analogous to a multi-elevation frost portfolio where Block 14 at 1,650 feet, Block 22 at 1,850 feet, and Block 31 at 2,200 feet are three correlated but distinct underlying processes. The basket structure allows a single policy to cover all three, with pricing reflecting the correlation matrix across elevations rather than naive summation.

MDPI MCA's work on hedging crop yields with weather derivatives closes the loop by combining stochastic temperature modeling with yield modeling and risk-neutral pricing. This is the full-stack framework: frost-hours → bud damage → yield impact → dollar loss → premium. Frontiers Plant Science's data-driven weather-index insurance design provides the data-driven design methods that turn stochastic future-hour probability bands into operational triggers.

The helm-charted yield forecast is what makes the model actually deployable. Without block-level telemetry, the settlement reference point is a regional weather station 14 miles downvalley — which is exactly the mismatch that made traditional crop insurance underprice high-gradient risk in the first place. With telemetry, settlement happens at the elevation band where the fruit actually sits.

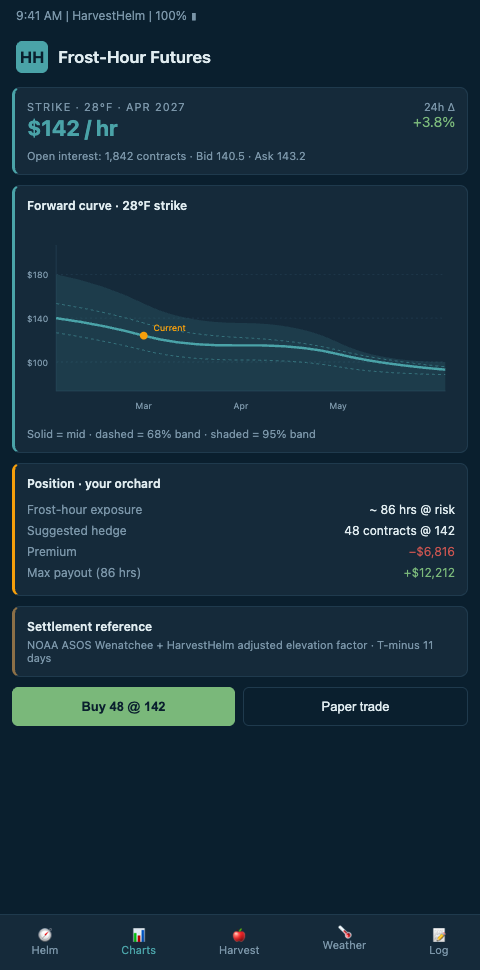

The premium math for a specific example. A 20-acre Honeycrisp block at 1,950 feet with a historical annual mean of 18 phenologically-weighted frost-hours and a standard deviation of 9 hours would price into a futures contract triggering at 30 hours with payouts of roughly $8,000 per hour above trigger. The premium on this contract — calibrated against a 10-year event distribution and the multi-year drift adjustment — would run roughly $3,800 per year. That covers the tail scenario where a compound cold year hits 45+ frost hours and the traditional APH policy is underwater.

Advanced Tactics for Variable-Elevation Contract Design

Three design choices separate a frost-hour futures model that actually pays out reliably from one that looks good on paper but fails growers in practice. First, threshold definition must match the phenological stage. A 28F frost-hour during dormancy is agronomic noise; a 28F frost-hour during pink bud is catastrophic. The futures model should index on phenologically-weighted frost-hours, giving more weight to hours accumulated during critical stages and discounting dormant-period exposure.

Second, basis risk minimization is the differentiator. The settlement sensor network must be dense enough that no block is more than 200 meters from a reference station. Every 500 meters of gap doubles basis risk, which is the distance between where damage happens and where the index measures. Dense on-orchard telemetry is the only way to keep basis risk in line.

Third, the contract should include a volatility layer, not just a flat strike. Simple "pay if frost-hours exceed X" contracts leave growers exposed to compound bad years. A layered structure — pay at X, pay more at Y, pay catastrophic at Z — matches the non-linear damage curve of real frost exposure. This connects directly to the critique that drives the insurance underpricing gradient discussion, and it scales into the broader slope-level yield underwriting framework. Tropical mango exporters are applying the same stochastic futures approach to fungal-disease risk; see disease pressure futures for the cross-niche parallel in humid-canopy risk transfer.

A fourth design tactic is reinsurance access. Individual orchards rarely have enough scale to directly access the institutional weather-derivatives market. Pooling frost-hour exposure across a regional group of mountain orchards creates a portfolio that is large enough to interest parametric reinsurers. HarvestHelm aggregates waitlisted orchards into regional pools (Hudson Valley, Green Mountains, Appalachian, Blue Ridge) and negotiates pool-scale contracts with reinsurance partners. Individual orchards get better pricing than they could access alone because their data and risk feed into a pool of similar-but-not-identical exposures, providing the diversification that reinsurers require.

The regulatory path requires careful navigation. Parametric weather derivatives sit in a different regulatory bucket than traditional APH crop insurance — they are typically structured as commodity contracts or specialty insurance products depending on jurisdiction. Growers should consult with an insurance broker familiar with parametric products before signing, and should ensure the contracts are stackable with existing APH rather than creating coverage conflicts. The stack-and-settle logic is that APH handles broad yield-loss, while the frost-hour futures handles the specific tail-risk on cold-event exposure that APH prices generically.

Settlement mechanics also matter operationally. The contract should settle on a clear, pre-defined calculation date (typically 10-14 days post-harvest completion) using the verified sensor data from the orchard's reference sensors. The sensor network itself must have tamper-resistance measures (tamper seals, cellular backup data paths, timestamp signing) that satisfy the underwriter's fraud-prevention requirements. HarvestHelm's hardware and data pipeline ship with these provisions by default, so the growerside lift is minimal.

Price Your Frost Risk the Way Utilities Price Temperature Risk

Variable-elevation apple orchards deserve the same risk-transfer infrastructure that utilities and breweries have used for decades. HarvestHelm builds the block-level telemetry foundation that makes frost-hour futures modeling actually work — dense sensors, elevation-band stratification, phenologically-weighted accumulation. Zero upfront cost, kilo-cut only on the cleared harvest. Mountain Apple Orchards growers on the HarvestHelm waitlist are the first pool for our 2026 futures-model pilot across Hudson Valley, Green Mountain, and Appalachian elevation bands. Stop self-insuring the high-gradient tail that legacy policies refuse to price correctly. Pilots signing before the next dormancy cycle enter the regional pool that lets individual orchards access institutional parametric reinsurers who require the diversification only a multi-orchard pool provides.

Day-one dashboard views show the probability distribution of frost-hours per elevation band, segmented into dormancy, pink-bud, and June-drop windows with phenologically-weighted exposure scores drawn against each. Onboarding includes the reference-sensor tamper seals, cellular backup, and timestamp signing required by parametric underwriters for fraud-prevention, so settlement mechanics satisfy the 10-to-14-day post-harvest calculation date without dispute. The kilo-cut contract settles only on cleared Honeycrisp, Gala, and Fuji tonnage whose elevation-band premium was paid through the pool, so a Block 22 Honeycrisp at 1,950 feet that carried 45 phenologically-weighted frost-hours under a 30-hour trigger costs us before it costs your operating cash flow. Stacking parametric frost-hour coverage alongside APH rather than replacing it gives growers the best of both policies without creating coverage conflicts at claim time.