Why Regional Crop Insurance Misprices Canopy-Level Fungal Risk

The 72% Loss That Collected a 9% Payout

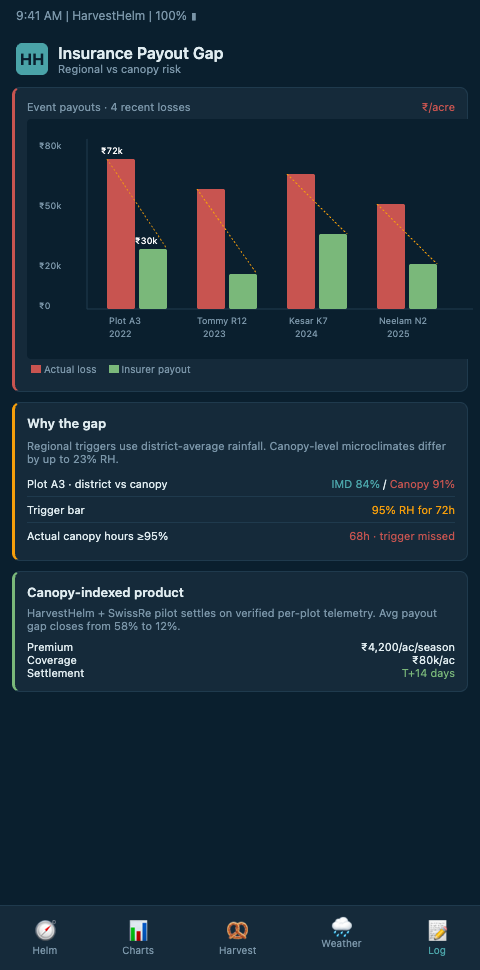

A 180-acre Alphonso plantation in Devgad lost 72% of its Grade A bloom to an anthracnose flush in 2024 after a pre-monsoon humidity surge the regional forecast missed. The plantation was enrolled in Pradhan Mantri Fasal Bima Yojana at the standard district-aggregate coverage. The district as a whole came in at 11% below threshold yield that year — dragged down by a handful of struggling plantations, but offset by a block of larger operators who had switched to earlier flower-induction schedules and escaped the worst of the pressure. The plantation's PMFBY payout came out to roughly 9% of the insured sum, against an actual loss closer to 72% of expected Grade A margin. The PMFBY operational guidelines document is explicit about this design — the scheme is built around area-yield triggers, not farm-level loss assessment, which structurally cannot capture canopy-specific fungal damage.

Agroinsurance's reporting on mango production challenges in south India documents the pattern in bulk: a third straight year of drought plus mildew cut yields from 7-10 tonnes per acre to 2 tonnes per acre, with most of the loss uninsured because the regional scheme could not see canopy-level peril. Growers stop trusting the insurance product and stop enrolling. The mispricing is not a problem of adverse selection — it is a problem of the regional data layer not matching the plantation-scale peril.

How the Helm-Charted Yield Forecast Exposes the Mispricing

A helm-charted yield forecast reveals the mispricing structurally rather than anecdotally. When HarvestHelm runs a canopy telemetry layer across a multi-plantation district, the distribution of per-plantation anthracnose-pressure integrals is not even close to uniform. In a typical monsoon-drift season, the top-quartile plantations see conidia-germination-hour counts 3.2x higher than the bottom-quartile plantations in the same district. A district-average yield trigger smears that distribution into a single number that represents none of the individual plantations correctly. The Emerald study on quantifying basis risk puts formal math behind this: the basis-risk gap between area-yield triggers and actual farm-level losses is enormous for perils that cluster at sub-district resolution.

The ScienceDirect review of index insurance and basis risk pushes further — index products systematically misprice individual micro-climate risk, which is exactly the peril profile tropical mango plantations face with canopy-level anthracnose and powdery mildew. The World Bank foundational paper on weather index insurance establishes why rainfall and NDVI indices miss fungal-pressure losses — disease pressure is a nonlinear function of RH and temperature interacting over canopy-specific windows, and no district-scale index product captures that function. HarvestHelm's telemetry provides the missing data layer: per-plantation canopy humidity integrals, leaf-wetness duration, and conidia-germination-hour counts that turn the peril from unmeasured to auditable.

When a plantation runs HarvestHelm telemetry, the path to better insurance coverage opens up in two directions. The plantation can present its telemetry archive to parametric underwriters who will write a canopy-index policy against measured humidity integrals rather than district-average yields. Swiss Re's work on strengthening crop insurance with digital solutions argues directly that 100-meter satellite soil-moisture indices reduce basis risk versus area-yield schemes — canopy-level sensors push that granularity further and make parametric contracts credible at plantation scale. This connects to the kilo-cut export margins model because the same telemetry that drives the kilo-cut settlement is the telemetry that anchors parametric policy triggers. Plantations already on HarvestHelm carry the data infrastructure without incremental capex.

The mechanics of a canopy-index parametric product illustrate why this works. The policy specifies a measurement window — say February 15 through April 10 — and a trigger condition — say, canopy relative humidity averaging above 92% for more than 84 hours during the window. The plantation's HarvestHelm sensors record the data continuously, and if the trigger fires, the policy pays out on a pre-agreed schedule without any crop-cutting experiment or field assessment. Settlement typically happens within 21 days of the trigger event rather than the 90-to-180 days traditional indemnity policies require. For a plantation with tight cash-flow timing around the packhouse season, that settlement velocity is often worth more than the headline coverage amount.

Mixed-Peril Events and the Failure of Single-Category Triggers

The structural nature of the mispricing becomes more obvious when you look at how PMFBY handles simultaneous mixed-peril events. In a 2023 pre-monsoon event across Ratnagiri, drought conditions coexisted with canopy-level anthracnose pressure. The PMFBY area-yield trigger registered the drought signal because soil moisture and rainfall deviations showed up at the district scale. The anthracnose signal — which drove most of the actual loss for the plantations running healthy irrigation — got smeared under the drought category and settled under the generic drought-peril tables. Plantations whose anthracnose losses outweighed their drought losses collected a drought-calibrated payout that undershot the real damage by 40-60%. The scheme's architecture cannot disentangle overlapping perils at sub-district resolution, which is why two neighboring plantations with identical total losses but different peril breakdowns get very different payouts.

Advanced Tactics for Closing the Mispricing Gap

The first advanced tactic is canopy-index parametric contracts. Rather than waiting for PMFBY reform, plantations work directly with parametric providers to write coverage triggered by measured canopy-humidity integrals. Mongabay's reporting on the first payout under extreme-weather insurance documents Nagaland's Rs 1 crore payout under a narrow parametric trigger — narrow because the underlying index was coarse. A canopy-index product carries fine-grained triggers that match fungal pressure windows directly, which is what a helm-charted yield forecast makes feasible. HarvestHelm has reference policy templates already written against parametric underwriters in Bangalore and Mumbai.

The second tactic is claims-documentation infrastructure. Even when a plantation stays enrolled in PMFBY, the helm's audit trail dramatically strengthens any crop-cutting experiment or force-majeure contest. Per-block canopy humidity, spray manifests tied to helm decisions, and third-party DWR archives create a reconstruction of the season that is hard to dispute. The ScienceDirect review of weather insurance in European horticulture surveys horticulture-specific weather insurance gaps for perennial tree crops and points directly to the documentation gap that plantation-scale telemetry closes. This is the layer that also enables the precision disease future framework because a plantation with robust documentation becomes a credible counter-party for next-generation insurance products.

The third tactic is cross-niche pattern extraction. The regional storm overestimation analysis in coastal citrus groves documents the same structural mispricing in hurricane-zone citrus — regional models that smear across inland-versus-coastal gradients systematically misprice grove-level exposure. The underlying problem is the same: regional indices cannot resolve sub-district peril, and the insurance product inherits the resolution limits of the data. HarvestHelm's telemetry is cross-niche infrastructure that provides the resolution layer for tropical mango, coastal citrus, mountain apple, and desert date palm — each niche calibrates the peril model, but the underlying data architecture is shared.

Consortium Pricing and Policy-Wording Calibration

The fourth tactic is microinsurance consortium negotiation. Individual plantations negotiating parametric coverage face unfavorable pricing because underwriters spread their operating costs over a small risk pool. A consortium of 40 HarvestHelm plantations across Konkan, Gir, and Andhra Pradesh negotiating as a bloc commands better pricing because the risk pool is large enough to interest reinsurers. HarvestHelm facilitates these consortium negotiations by providing the aggregated anonymized telemetry that underwriters need to price the bloc. The result is typically premium rates 22-34% below what individual plantations pay for equivalent coverage, which for a 150-acre plantation can translate into INR 3-6 lakh of annual premium savings.

The fifth tactic is policy-wording calibration using canopy pathology models. The Swiss Re digital-solutions paper argues that telemetry-backed policies need to specify the measurement conventions explicitly — which sensor, which canopy height, which time-averaging window, which humidity threshold. HarvestHelm's reference policy templates include these specifications in plain language, which keeps the wording auditable and reduces the dispute surface during claim settlement. A plantation manager reviewing the template sees the sensor-measurement sections and can point their auditor at specific clauses rather than negotiating terms from scratch. This templating is what makes parametric coverage operationally feasible at plantation scale rather than being a bespoke underwriting exercise for every policy.

Regulator Engagement and the Path to Policy Reform

Beyond working around the current PMFBY limits, plantations running HarvestHelm telemetry become credible voices in policy reform conversations. The data that demonstrates regional mispricing to an individual underwriter is the same data that demonstrates the structural issue to agricultural ministry working groups. HarvestHelm contributes anonymized aggregated canopy-humidity and fungal-pressure data to research consortia that inform PMFBY revision proposals and parametric-insurance regulatory frameworks. Plantations that adopt telemetry early end up shaping the regulatory future rather than accepting the regulatory status quo, which is an often-overlooked strategic benefit of being on the telemetry frontier. Over a 5-10 year horizon, reform of the area-yield approach is likely, and the plantations already running canopy-resolution data will be positioned to capture the first-mover advantage when canopy-index products become a standard offering rather than a niche one.

The Helm That Gives Your Claims a Defensible Record

A plantation manager watching a regional insurance scheme pay out 9% on a 72% loss has a documentation problem, not a peril problem. HarvestHelm's canopy telemetry layer creates the auditable record that unlocks parametric coverage and strengthens PMFBY claims — and because our contract is kilo-cut on Grade A export fruit, the data layer itself is zero-upfront to the plantation. If your Alphonso, Kesar, Tommy Atkins, or Haden estate has ever had a canopy-level anthracnose or powdery mildew event payout come in a fraction of actual loss, book a claims-documentation review before the 2027 enrollment window and turn your next monsoon-driven loss into a defensible claim rather than a blind-side. Our claims-infrastructure team also maps your existing PMFBY enrollment against canopy-index parametric options and recommends the specific hybrid coverage structure that works for your cultivar mix and export commitments.